Strategy Parameter Optimization

After developing a trading strategy, how do you find the best combination of conditions? The finlab.optimize module provides the sim_conditions() function to automatically test all condition combinations and visually compare performance, helping you identify the strongest strategy.

Why Strategy Optimization?

When developing trading strategies, we often have multiple screening conditions:

- Technical: Moving average crossovers, new highs, RSI indicators

- Fundamental: P/E ratio, revenue growth, profitability

- Institutional: Institutional buying, margin balance changes

Each condition alone may produce mediocre performance, but combining multiple conditions may yield unexpected results. Manually testing all combinations is extremely time-consuming; sim_conditions() automates this process.

Quick Start

Basic Example: All Combinations of 3 Conditions

Suppose we have 3 screening conditions:

from finlab import data

from finlab.backtest import sim

from finlab.optimize.combinations import sim_conditions

close = data.get("price:收盤價")

rev = data.get('monthly_revenue:當月營收')

營業利益成長率 = data.get('fundamental_features:營業利益成長率')

# Define 3 conditions

c1 = (close > close.average(20)) & (close > close.average(60)) # Technical: MA breakout

c2 = 營業利益成長率 > 0 # Fundamental: profit growth

c3 = rev.average(3) / rev.average(12) > 1.1 # Fundamental: revenue acceleration

# Set exit condition

exits = close < close.average(20)

# Conditions dictionary, keys are condition names

conditions = {'c1': c1, 'c2': c2, 'c3': c3}

# Test all combinations

report_collection = sim_conditions(

conditions=conditions,

hold_until={'exit': exits, 'stop_loss': 0.1}, # Exit when below MA, 10% stop-loss

resample='M', # Monthly rebalancing

position_limit=0.1, # Max 10% per stock

upload=False # Don't upload to cloud

)

This code automatically tests the following 7 combinations:

c1(technical only)c2(profit growth only)c3(revenue acceleration only)c1 & c2(technical + profit growth)c1 & c3(technical + revenue acceleration)c2 & c3(profit growth + revenue acceleration)c1 & c2 & c3(all three conditions)

Visual Performance Comparison

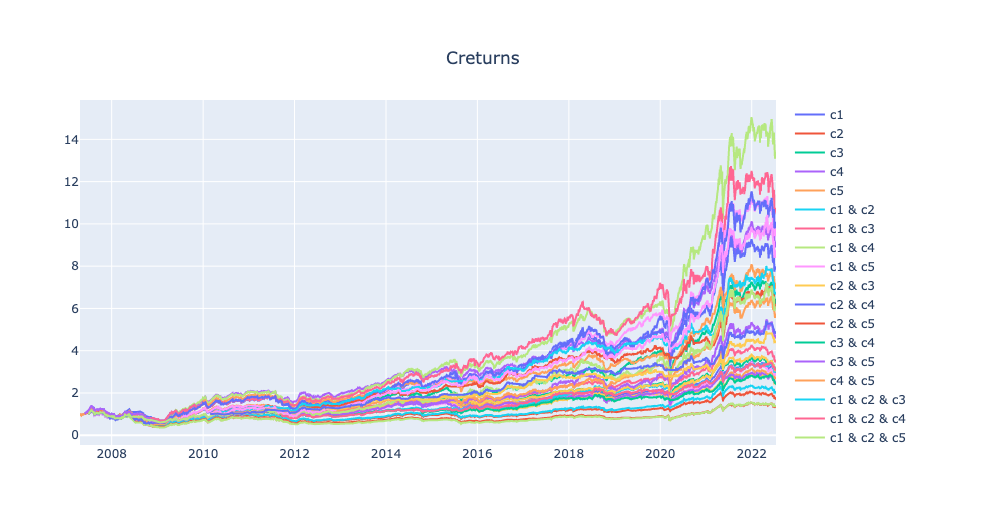

1. Cumulative Return Line Chart

Compare the equity curves of each combination:

From the chart, you can see which combination has the best long-term performance and the stability of each combination.

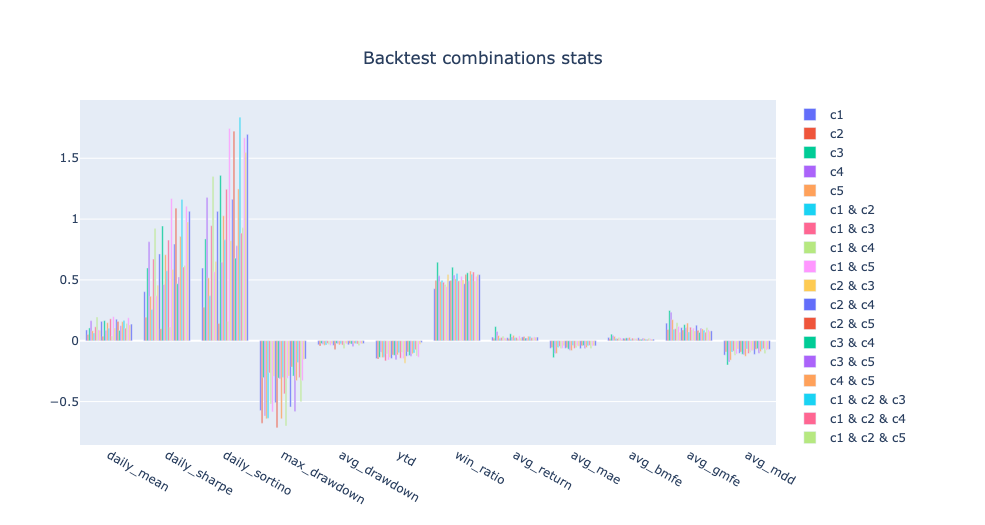

2. Grouped Bar Chart of Metrics

Displays 12 key metrics side by side for all combinations for quick comparison.

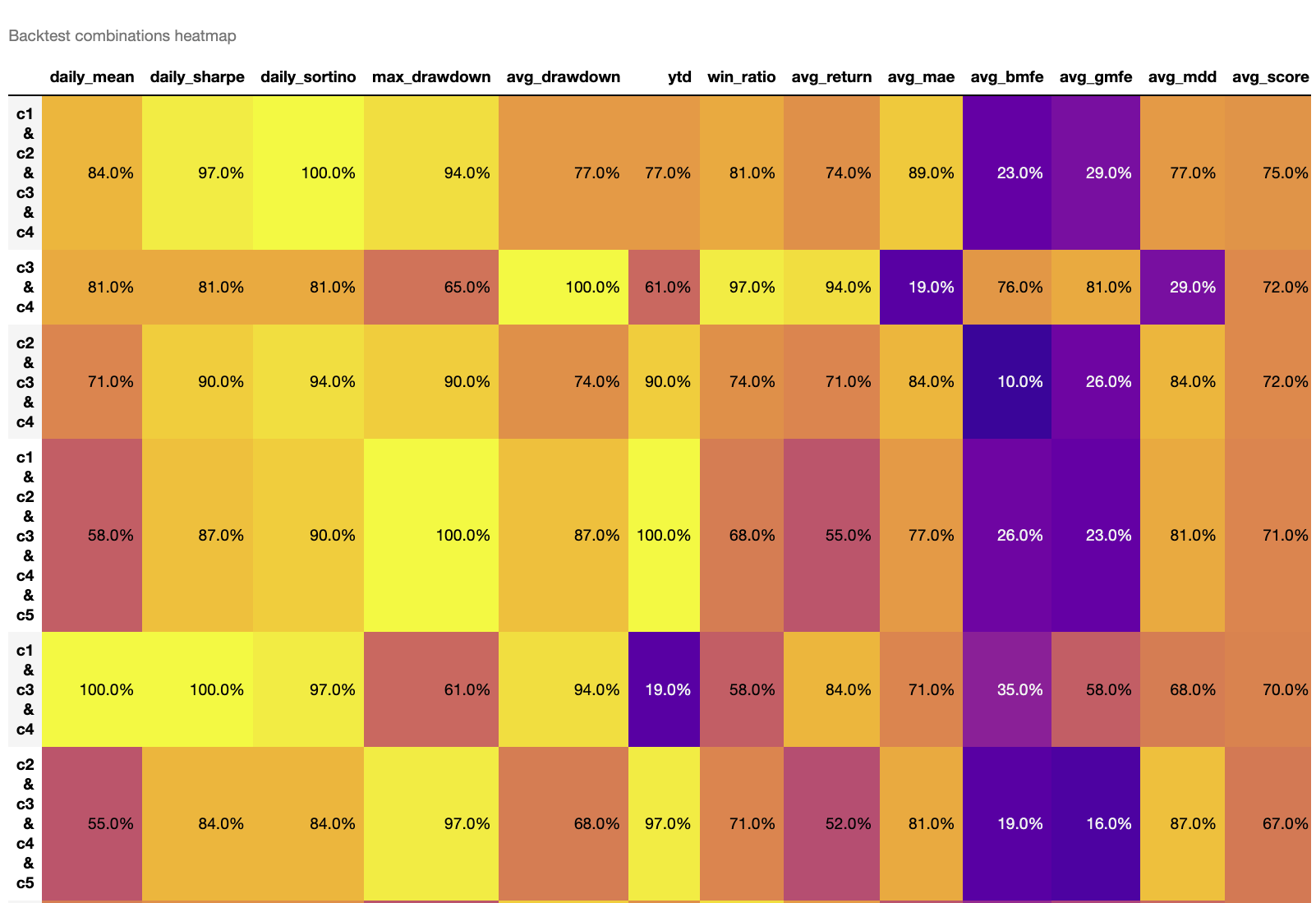

3. Metric Ranking Heatmap

The heatmap uses color intensity to represent the percentile ranking (0-100%) of each metric. Higher values indicate better rankings:

- avg_score: Average score across all metrics; higher scores indicate better overall performance

- Sorted by

avg_scorein descending order by default, with the best combination at the top - Brighter colors (yellow) indicate higher rankings for that metric

How to interpret the heatmap

- Look for the combination with the highest avg_score (usually at the top)

- Check that the combination performs well on key metrics (Sharpe ratio, win rate, max drawdown)

- Avoid combinations with especially poor metrics (dark purple)

Get Detailed Performance Metrics

Returns a DataFrame with 12 metrics:

Strategy-Level Metrics

| Metric | Description | Direction |

|---|---|---|

daily_mean |

Annualized return | Higher is better |

daily_sharpe |

Annualized Sharpe ratio (risk-adjusted return) | Higher is better |

daily_sortino |

Annualized Sortino ratio (downside risk-adjusted return) | Higher is better |

max_drawdown |

Maximum drawdown (negative value) | Smaller absolute value is better |

avg_drawdown |

Average drawdown (negative value) | Smaller absolute value is better |

Trade-Level Metrics

| Metric | Description | Direction |

|---|---|---|

win_ratio |

Win rate per trade | Higher is better |

avg_return |

Average profit per trade | Higher is better |

avg_mae |

Average MAE per trade (negative value) | Smaller absolute value is better |

avg_bmfe |

Average BMFE (MFE before MAE) per trade | Higher is better |

avg_gmfe |

Average global MFE per trade | Higher is better |

avg_mdd |

Average max drawdown per trade (negative value) | Smaller absolute value is better |

Meaning of avg_bmfe

avg_bmfe represents how high the stock price went before the stop-loss was triggered. The higher this value, the more opportunity there is to take profit before the stop-loss -- an important reference for optimizing take-profit points.

Advanced Example: Optimization with 5 Conditions

When conditions increase to 5, the number of combinations reaches 31 (2^5 - 1). Manual testing is very difficult, but sim_conditions() handles it easily:

from finlab import data

from finlab.optimize.combinations import sim_conditions

close = data.get("price:收盤價")

pe = data.get('price_earning_ratio:本益比')

rev = data.get('monthly_revenue:當月營收').index_str_to_date()

rev_ma3 = rev.average(3)

rev_ma12 = rev.average(12)

# 5 conditions

c1 = (close > close.average(20)) & (close > close.average(60)) # MA bullish alignment

c2 = (close == close.rolling(20).max()) # 20-day new high

c3 = pe < 15 # Low P/E

c4 = rev_ma3 / rev_ma12 > 1.1 # Revenue acceleration

c5 = rev / rev.shift(1) > 0.9 # Monthly revenue change > -10%

exits = close < close.average(20)

conditions = {'c1': c1, 'c2': c2, 'c3': c3, 'c4': c4, 'c5': c5}

report_collection = sim_conditions(

conditions=conditions,

hold_until={'exit': exits, 'stop_loss': 0.1},

resample='M',

position_limit=0.1,

upload=False

)

# View heatmap to quickly find the best combination

report_collection.plot_stats('heatmap')

Interpreting Results

Suppose the heatmap shows c1 & c3 & c4 has the highest avg_score:

- Check cumulative return curve: Confirm steady NAV growth

- Check key metrics:

- Sharpe ratio > 1.5? (Is risk-adjusted return sufficient?)

- Max drawdown < -30%? (Can you tolerate the worst case?)

- Win rate > 50%? (Is the trade win rate reasonable?)

- Analyze combination meaning:

c1 & c3 & c4represents "technical breakout + cheap valuation + revenue growth" -- this combination has clear business logic

Customize Displayed Metrics

If you only care about specific metrics, use the indicators parameter:

# Show only return, Sharpe ratio, and max drawdown

report_collection.plot_stats('bar', indicators=['daily_mean', 'daily_sharpe', 'max_drawdown']).show()

# Sort heatmap by Sharpe ratio

report_collection.plot_stats('heatmap', heatmap_sort_by='daily_sharpe')

# Sort heatmap by multiple metrics

report_collection.plot_stats('heatmap', heatmap_sort_by=['daily_sharpe', 'win_ratio'])

Combining with Stop-Loss/Take-Profit Optimization

The hold_until parameter of sim_conditions() supports various exit logics:

# 1. Exit signal only

hold_until = {'exit': exits}

# 2. Exit signal + stop-loss

hold_until = {'exit': exits, 'stop_loss': 0.1}

# 3. Exit signal + take-profit

hold_until = {'exit': exits, 'take_profit': 0.2}

# 4. Exit signal + stop-loss + take-profit

hold_until = {'exit': exits, 'stop_loss': 0.1, 'take_profit': 0.2}

# 5. Exit signal + stop-loss (trailing stop requires trail_stop in sim())

hold_until = {'exit': exits, 'stop_loss': 0.1}

# Combined with: sim_conditions(..., trail_stop=0.15)

Stop-loss/take-profit setting suggestions

- First run

report.display_mae_mfe_analysis()to analyze volatility characteristics - Set the stop-loss point based on the MAE distribution (avoid over-stopping)

- Set the take-profit point based on the MFE distribution (ensure profits are realized)

- Use

sim_conditions()to test different stop-loss/take-profit combinations

FAQ and Best Practices

Q1: Too many combinations causing long computation time?

When the number of conditions > 6, combinations exceed 63. Suggestions:

- Pre-filter important conditions: Use single-condition backtests to remove poorly performing conditions

- Test in batches: Separate conditions into technical, fundamental, and institutional groups

- Use longer resample: Switch to

resample='Q'(quarterly) to reduce computation

Q2: How to avoid overfitting?

- Out-of-sample testing: Optimize on historical data, validate on recent data

- Avoid too many conditions: Be especially careful when conditions > 5

- Check combination logic: Does the best combination have business logic support?

- Evaluate multiple metrics: Don't just look at returns; also consider Sharpe ratio, drawdown, and win rate

Q3: What if conditions have inconsistent data frequencies?

FinLab automatically aligns data frequencies:

# Daily data

close = data.get("price:收盤價") # Updated daily

# Monthly data

rev = data.get('monthly_revenue:當月營收') # Updated monthly

# Quarterly data

eps = data.get('financial_statement:每股盈餘') # Updated quarterly

# Mixing frequencies works fine; FinLab auto forward-fills

conditions = {

'c1': close > close.average(20),

'c2': rev.average(3) > rev.average(12),

'c3': eps > 0

}

Q4: Why do some combinations fail backtesting?

Possible causes:

- Conditions too strict: No stocks meet the intersection criteria

- Missing data: Some conditions have insufficient data coverage

- Insufficient memory: Too many combinations cause OOM

Check the log for specific error messages.

Q5: How to access a specific combination's backtest report?

# report_collection.reports is a dict

print(report_collection.reports.keys())

# Output: dict_keys(['c1', 'c2', 'c3', 'c1 & c2', 'c1 & c3', ...])

# Get a specific combination's report

report = report_collection.reports['c1 & c3']

report.display()

Practical Workflow Recommendations

- Define candidate conditions (5-8)

- Single-condition backtest: Confirm each condition has basic performance

- Use

sim_conditions(): Test all combinations - Visual analysis:

- Use heatmap to find the top 3 combinations

- Use line charts to confirm NAV stability

- Use bar charts to compare key metrics

- Deep dive into top 3:

- Run MAE/MFE analysis

- Check liquidity risk

- Run out-of-sample tests

- Select final strategy: Consider performance, risk, and logical soundness