Strategy Analysis Modules

After backtesting, looking only at the cumulative return curve and Sharpe ratio may not be comprehensive enough. The finlab.analysis module provides 6 built-in analysis tools that evaluate strategy quality from multiple angles including liquidity risk, volatility characteristics, and period stability, helping you make more informed trading decisions.

Overview

FinLab includes the following 6 analysis modules:

| Module | Purpose | Use Case |

|---|---|---|

| LiquidityAnalysis | Liquidity risk assessment | Large capital strategies, low-liquidity assets |

| MaeMfeAnalysis | Volatility analysis (MAE/MFE) | Optimizing stop-loss/take-profit, understanding strategy characteristics |

| PeriodStatsAnalysis | Period stability analysis | Reviewing yearly, monthly, and recent performance |

| InequalityAnalysis | Inequality factor analysis | Checking if strategy relies on specific stocks |

| AlphaBetaAnalysis | Alpha/Beta analysis | Measuring excess return and market correlation |

| DrawdownAnalysis | Drawdown analysis | Understanding max drawdown timing and magnitude |

Basic Usage

All analysis modules use the same calling convention:

from finlab import data

from finlab.backtest import sim

# Complete backtest

close = data.get('price:收盤價')

position = close > close.average(20)

report = sim(position, resample='M')

# Run analysis - Method 1: Using module name (string)

report.run_analysis('LiquidityAnalysis', required_volume=100000)

# Run analysis - Method 2: Using module instance

from finlab.analysis.liquidityAnalysis import LiquidityAnalysis

report.run_analysis(LiquidityAnalysis(required_volume=100000))

Method 1 is recommended

Passing the module name as a string is more concise, and FinLab handles module loading automatically.

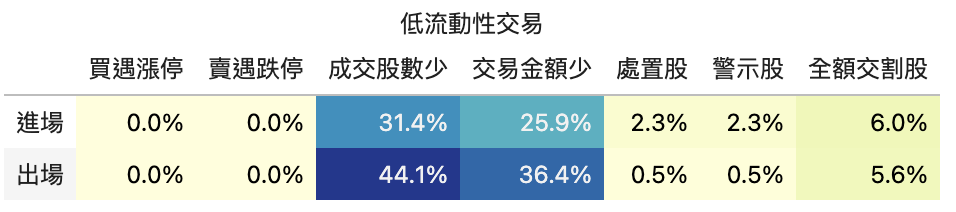

1. LiquidityAnalysis - Liquidity Risk Assessment

Description

Detects whether the strategy encounters liquidity issues during entry/exit, including:

- Insufficient volume: Daily trading volume below requirements

- Insufficient turnover: Daily trading value below requirements

- Price limits: Buying at upper limit or selling at lower limit (unable to execute)

- Alert/Disposition/Full-delivery stocks: High-risk securities with trading restrictions

Parameters

LiquidityAnalysis(

required_volume=200000, # Required daily trading volume (default: 200,000 shares)

required_turnover=1000000 # Required daily turnover (default: 1,000,000)

)

Usage Example

Interpreting Output

The table shows the probability of each risk item occurring at entry and exit:

| Risk Item | entry | exit | Description |

|---|---|---|---|

| buy_high | 5.2% | 1.3% | Percentage of trades buying at or near the upper price limit |

| sell_low | 0.8% | 4.5% | Percentage of trades selling at or near the lower price limit |

| low_volume_stocks | 12.1% | 10.3% | Percentage of trades with insufficient volume |

| low_turnover_stocks | 8.7% | 7.2% | Percentage of trades with insufficient turnover |

| Alert stocks | 2.1% | 1.8% | Percentage of trades involving alert stocks |

| Disposition stocks | 0.5% | 0.3% | Percentage of trades involving disposition stocks |

| Full-delivery stocks | 0.2% | 0.1% | Percentage of trades involving full-delivery stocks |

Risk threshold suggestions

buy_highorsell_low> 10%: Orders may not execute smoothlylow_volume_stocks> 20%: Large capital may not fully deployDisposition stocks> 5%: Strategy may be targeting high-risk securities

Decision Recommendations

- Insufficient liquidity: Add screening conditions (e.g., "volume > 1000 lots")

- Frequent price limit hits: Adjust entry/exit timing (e.g., use open price instead of close)

- Too many alert/disposition stocks: Add risk control conditions to exclude high-risk securities

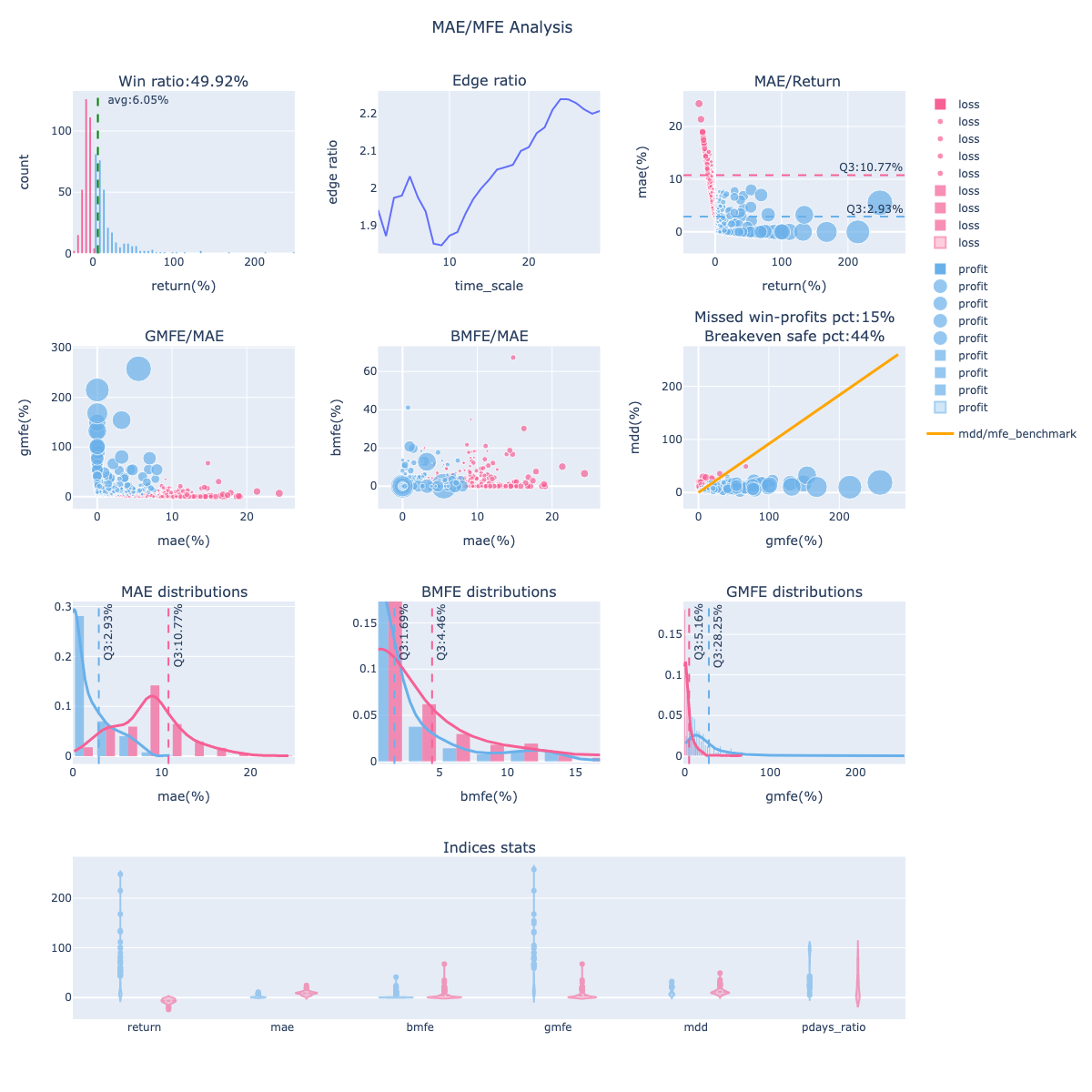

2. MaeMfeAnalysis - Volatility Analysis

Description

MAE/MFE analysis is the core tool for optimizing stop-loss/take-profit:

- MAE (Maximum Adverse Excursion): Maximum adverse movement during holding period (max loss)

- BMFE (Before-MAE MFE): Maximum favorable movement before MAE occurred

- GMFE (Global MFE): Maximum favorable movement during holding period (max profit)

- MDD (Maximum Drawdown): Maximum drawdown during holding period

Through 12 subplots, gain a comprehensive understanding of each trade's volatility characteristics.

Parameters

MaeMfeAnalysis(

violinmode='group', # Violin plot mode: 'group' or 'overlay'

mfe_scatter_x='mae' # MFE scatter plot X-axis: 'mae' or 'return'

)

Usage Example

# Method 1: Using the display_mae_mfe_analysis() shortcut

report.display_mae_mfe_analysis()

# Method 2: Using run_analysis()

report.run_analysis('MaeMfeAnalysis', violinmode='group')

12 Subplot Descriptions

Row 1

- Win Ratio: Trade win rate distribution (profit vs loss histogram)

- Blue: profitable trades, Pink: losing trades

-

Green dashed line: average return

-

Edge Ratio: MFE/MAE ratio at different holding periods

- Value > 1 means profit magnitude exceeds loss magnitude

-

Observe the strategy's "edge time window"

-

MAE vs Return: Relationship between MAE and final return

- Horizontal dashed line: MAE 75th percentile (Q3)

- Used for setting stop-loss points

Row 2

- GMFE vs MAE: Maximum profit vs maximum loss

- Q3 dashed lines: Range of 75% of trades' GMFE and MAE

-

Used for evaluating take-profit potential

-

BMFE vs MAE: Maximum profit before MAE occurred

- Higher values mean more opportunity to take profit before stop-loss triggers

-

Used for optimizing "trailing stop" strategies

-

MDD vs GMFE: Maximum drawdown vs maximum profit

- Orange line: MDD = GMFE baseline

- Points below: GMFE > MDD (good signal, trailing stop viable)

- Points above: MDD > GMFE (bad signal, missing profits)

Row 3

7-9. MAE/BMFE/GMFE Distribution: Distribution and density of each metric - Histogram + density curve - Blue: profitable trades, Pink: losing trades - Q3 dashed line: 75th percentile

Row 4

- Indices Stats (Violin Plot): Statistical distribution of 6 key metrics

- return, mae, bmfe, gmfe, mdd, pdays_ratio

- group mode: Shows profit/loss trade differences separately (recommended)

- overlay mode: All trades overlaid

Decision Recommendations

Optimize stop-loss/take-profit based on MAE/MFE analysis:

Setting Stop-Loss

# 1. Check MAE 75th percentile (Q3)

trades = report.get_trades()

mae_q3 = trades['mae'].quantile(0.75) # e.g., -8.5%

# 2. Set stop-loss slightly wider than Q3 to avoid over-stopping

stop_loss = abs(mae_q3) * 1.2 # Set to 10%

Setting Take-Profit

# Check GMFE 75th percentile

gmfe_q3 = trades['gmfe'].quantile(0.75) # e.g., 15%

# Set take-profit

take_profit = gmfe_q3 * 0.8 # Set to 12%, ensuring most profits are captured

Trailing Stop Decision

If the "MDD vs GMFE" chart shows:

- Missed Win-profits PCT < 20%: Trailing stop is suitable

- Missed Win-profits PCT > 40%: Trailing stop is not suitable (exits too early, missing larger gains)

# Use trailing stop (via sim()'s trail_stop parameter)

position = position.hold_until(

exit=exits,

stop_loss=0.1

)

report = sim(position, resample='M', trail_stop=0.08) # Exit on 8% pullback

3. PeriodStatsAnalysis - Period Stability Analysis

Description

Analyzes strategy performance across different periods (yearly, monthly, recent) and compares with a benchmark to verify stability.

Usage Example

Interpreting Output

Produces multiple tables including:

1. Overall Stats

Compares strategy vs benchmark on daily, monthly, and yearly metrics:

| Metric | benchmark | strategy |

|---|---|---|

overall_daily / calmar_ratio |

0.149 | 0.066 |

overall_daily / sharpe_ratio |

0.532 | 0.306 |

overall_monthly / return |

0.084 | 0.048 |

2. Yearly Stats

Heatmap showing 7 metrics per year (calmar_ratio, sharpe_ratio, return, volatility, etc.).

3. Recent Stats

Shows performance for M (month), Q (quarter), HY (half-year), Y (year), 3Y (three years).

Decision Recommendations

- Strategy sharpe_ratio < benchmark: Risk-adjusted return is worse than the market; improvement needed

- Some years perform very poorly: Check if specific market conditions were encountered (e.g., bear market)

- Recent performance significantly declined: Strategy may be failing; re-optimization needed

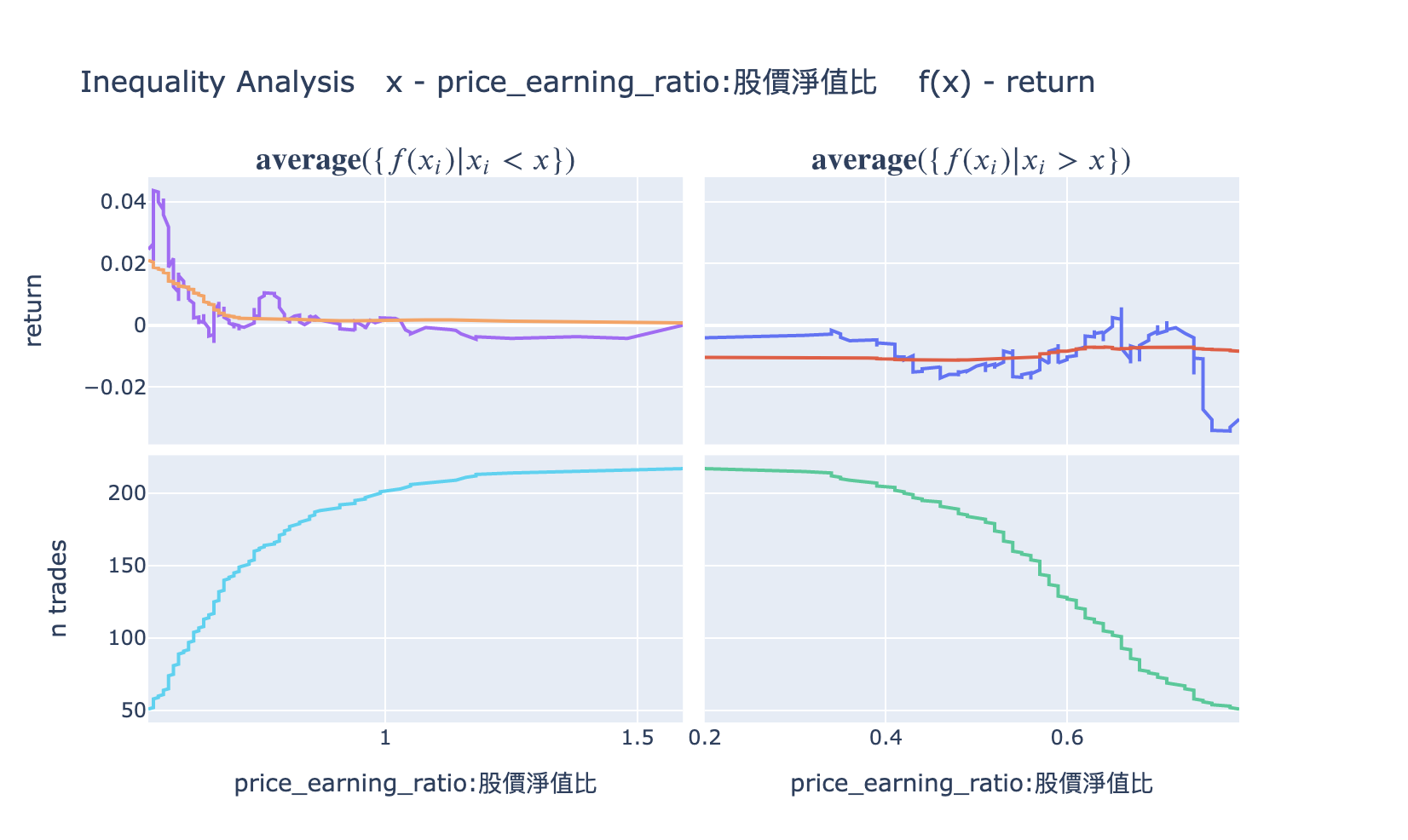

4. InequalityAnalysis - Inequality Factor Analysis

Description

Checks whether strategy returns are overly concentrated in a few stocks, evaluating strategy robustness.

Usage Example

Interpreting Output

Produces two charts:

- Cumulative Returns by Stock: Cumulative contribution curve by stock

-

If the curve reaches 80% within the top 10% of stocks, returns are overly concentrated

-

Gini Coefficient: Gini coefficient (0-1)

- Close to 0: Returns are evenly distributed (good)

- Close to 1: Returns are extremely concentrated (high risk)

Decision Recommendations

- Gini > 0.7: Strategy is overly dependent on a few stocks; diversification needed

- Top 5% stocks contribute > 50% of returns: Remove these stocks and test strategy robustness

5. AlphaBetaAnalysis - Alpha/Beta Analysis

Description

Measures strategy performance relative to a benchmark index:

- Alpha: Excess return (the strategy's unique value)

- Beta: Market sensitivity (correlation with the market)

Usage Example

Interpreting Output

Shows three sections:

-

Overall Summary -- Alpha and Beta overview:

Metric Value Description Alpha 5.00% Annualized excess return (true contribution after removing market risk) Beta 0.80 Market sensitivity (market up 1%, strategy expected up 0.8%) -

Yearly Alpha/Beta -- Annual Alpha and Beta breakdown to observe strategy stability

-

Recent Alpha/Beta -- Performance for full period, recent 1M, 3M, 6M, 1Y

To get raw data (dict):

result = report.run_analysis('AlphaBetaAnalysis', display=False)

# result['overall'] -> {'alpha': 0.05, 'beta': 0.8}

# result['yearly'] -> {'alpha': [...], 'beta': [...], 'year': [...]}

# result['recent'] -> {'alpha': [...], 'beta': [...], 'ndays': [...]}

Decision Recommendations

- Alpha > 0: Strategy has excess returns; worth executing

- Alpha < 0: Strategy underperforms the benchmark; improvement needed

- Beta > 1.5: Strategy volatility is extremely high; high risk

- Beta < 0: Strategy is negatively correlated with the market (suitable for hedging)

6. DrawdownAnalysis - Drawdown Analysis

Description

Detailed analysis of all drawdown events:

- Maximum drawdown magnitude and timing

- Average drawdown magnitude

- Drawdown duration

Usage Example

Interpreting Output

Produces tables and charts:

- Drawdown Events Table: Detailed information for all drawdown events

- start_date: Drawdown start date

- end_date: Drawdown end date

- duration: Duration in days

-

max_dd: Maximum drawdown magnitude

-

Drawdown Plot: Drawdown time series chart

Decision Recommendations

- Max drawdown > -50%: Risk is too high; additional risk controls needed

- Drawdown duration > 1 year: Strategy may be ineffective long-term

- Frequent recent drawdowns: Market conditions may have changed; re-evaluate strategy

Custom Analysis Modules

If built-in analysis is insufficient, you can inherit the Analysis class to develop custom analysis.

Basic Example: Industry Analysis

Analyze the industry of each trade:

from finlab import data

from finlab.analysis import Analysis

class IndustryAnalysis(Analysis):

def calculate_trade_info(self, report):

"""Calculate industry information for each trade"""

industry = data.get('etl:industry')

return [

['Industry', industry, 'entry_sig_date']

]

def analyze(self, report):

"""Analyze industry distribution"""

trades = report.get_trades()

industry_return = trades.groupby('Industry@entry_sig_date')['return'].agg(['count', 'mean'])

self.result = industry_return.sort_values('mean', ascending=False)

return self.result.to_dict()

def display(self):

"""Display analysis results"""

return self.result

# Use custom analysis

report.run_analysis(IndustryAnalysis())

Advanced Example: Monthly Win Rate Analysis

Analyze whether win rates differ by month:

class MonthlyWinRateAnalysis(Analysis):

def analyze(self, report):

trades = report.get_trades()

trades['entry_month'] = pd.to_datetime(trades['entry_date']).dt.month

monthly_stats = trades.groupby('entry_month').agg({

'return': ['count', lambda x: (x > 0).mean(), 'mean']

}).round(3)

monthly_stats.columns = ['Trade Count', 'Win Rate', 'Average Return']

self.result = monthly_stats

return self.result.to_dict()

def display(self):

import plotly.express as px

fig = px.bar(self.result, y='Win Rate', title='Monthly Win Rate Analysis')

return fig

# Usage

report.run_analysis(MonthlyWinRateAnalysis())

Analysis Class API

When inheriting the Analysis class, you can override the following methods:

class Analysis:

def is_market_supported(self, market):

"""Check if the market is supported

Returns:

bool: True if supported, False otherwise

"""

return True

def calculate_trade_info(self, report):

"""Calculate additional trade information

Returns:

list: Format is [[field_name, data DataFrame, date column used], ...]

Examples:

return [

['Industry', industry_data, 'entry_sig_date'],

['Market Cap', market_cap, 'entry_date']

]

"""

return []

def analyze(self, report):

"""Execute analysis logic

Args:

report: Backtest report object

Returns:

dict: Analysis results (for cloud upload)

"""

pass

def display(self):

"""Display analysis results

Returns:

Visualization object (Plotly Figure or Pandas Styler recommended)

"""

pass

Purpose of calculate_trade_info

calculate_trade_info() executes before analyze(), automatically adding additional information to the report.get_trades() DataFrame.

For example, returning [['Industry', industry, 'entry_sig_date']] adds an 'Industry@entry_sig_date' column to trades.

Combining Multiple Analysis Modules

In practice, running multiple analyses simultaneously is recommended:

from finlab import data

from finlab.backtest import sim

# Complete backtest

close = data.get('price:收盤價')

position = close > close.average(20)

report = sim(position, resample='M')

# 1. Liquidity assessment

report.run_analysis('LiquidityAnalysis', required_volume=100000)

# 2. Volatility analysis

report.display_mae_mfe_analysis()

# 3. Period stability analysis

report.run_analysis('PeriodStatsAnalysis')

# 4. Alpha/Beta analysis

report.run_analysis('AlphaBetaAnalysis')

# 5. Custom industry analysis

report.run_analysis(IndustryAnalysis())

Best Practices

1. Standard Analysis Workflow

After each strategy backtest, the following checks are recommended:

# Step 1: Basic performance review

report.display()

# Step 2: Liquidity risk (must-check for large capital)

if capital > 1000000:

report.run_analysis('LiquidityAnalysis', required_volume=100000)

# Step 3: Volatility analysis (must-do, for optimizing stop-loss/take-profit)

report.display_mae_mfe_analysis()

# Step 4: Period stability (check long-term stability)

report.run_analysis('PeriodStatsAnalysis')

# Step 5: Alpha/Beta (check for excess return)

report.run_analysis('AlphaBetaAnalysis')

2. Analysis Focus by Strategy Type

| Strategy Type | Key Analysis Module |

|---|---|

| Short-term trading (intraday, weekly) | MaeMfeAnalysis (optimize stop-loss/take-profit) |

| Long-term investing (monthly, quarterly) | PeriodStatsAnalysis (check long-term stability) |

| Large capital strategies (> 10M) | LiquidityAnalysis (avoid liquidity risk) |

| Market neutral strategies | AlphaBetaAnalysis (confirm Beta close to 0) |

| High-frequency trading | DrawdownAnalysis (confirm drawdowns are manageable) |

3. Analysis Result Decision Tree

Backtest Complete

+- Liquidity risk > 20%?

| +- Yes -> Add volume screening conditions

| +- No -> Continue

+- Sharpe ratio < 1?

| +- Yes -> Optimize screening conditions or stop-loss/take-profit

| +- No -> Continue

+- Max drawdown > -30%?

| +- Yes -> Add risk controls (stop-loss, position sizing)

| +- No -> Continue

+- Alpha < 0?

| +- Yes -> Strategy has no excess return; needs redesign

| +- No -> Continue

+- All checks passed -> Proceed to out-of-sample testing